Recently, we have probably all seen the headlines regarding the growing market of invoice factoring. It has become an interesting market, and a reliable source for SMEs to stabilize their financials.

It is interesting to note that even though news regarding invoice factoring reaches huge headlines, invoice factoring or financing is not as popular as it would seem. SMEs are all fully aware that maintaining a healthy and steady cash flow is a hard task to achieve. Invoicing software which enables for payment automation will generally result in your invoices getting paid faster, and can help SMEs maintain a decent cash-flow. But what happens, when your business is in dire need of quick cash? When money is required to start a new project, to purchase supplies, to pay taxes, or because payroll is due?

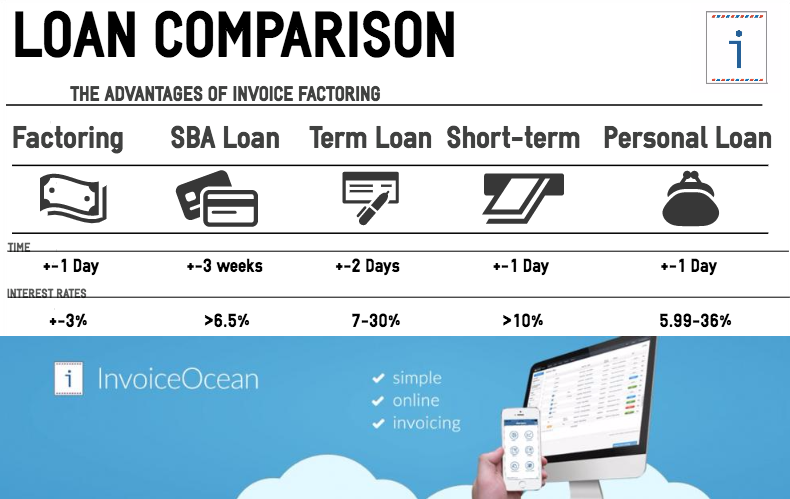

Many companies will look towards loans or perhaps even a Merchant cash advance to finance their operations and to quickly obtain some cash. The table below shows the possibilities, which can originally be found

here.

The interest rates for Invoice financing/discounting and for invoice factoring are incredibly attractive, though they do significantly depend on the date of payment. There are downsides to this type of SME cash-flow maintenance, with the most obvious one being the fact that you will not obtain full value for your work. It is technically a loan, after all, so your loan extenders have to have some sort of collateral and profit. The good thing about the collateral is that it is literally an invoice, and hence SMEs do not risk losing more when defaulting.

In general, businesses that opt for invoicing factoring can expect to receive an amount of cash up front which ranges between 50-90% of the total invoice value. The rest will be paid after the factoring company obtains the payment. To better illustrate the process, here is an example of it in practice.

Company A specializes in B2B construction, it has 5 employees on its payroll. And has just completed a massive project, the biggest to this date. The project required a lot of initial investment, but the profits would be well worth the investment. Using InvoiceOcean, company A’s CEO John has quickly dispatched an invoice to Company B, which had tasked Company A with the project. Company A has done everything to ensure a smooth payment procedure, the invoice looks professional, and has a clearly stated payment date. Unfortunately, after the 14 day period has passed, Company B still has not completed the payment. A reminder is dispatched automatically but John is starting to worry.

The end of the month is approaching, new projects have to be financed, and his employees will expect payment. John has never been late with paying salaries and has no intention to do so. He reaches out to an Invoice factoring company and after explaining the situation they have decided on the following;

- 80% of the $500,000 (total invoice) will be paid within the day

- 3% will be the go to Fee for the Factoring company

- 1% additional fee per outstanding week.

Company A receives; $400,000 the same day that the agreement was established. John can now finance his expenses, pay his employee, and even has enough left as a safety net for further projects.

Finally, two weeks after the due date, Company B transfers the money to the Factoring company for the invoice. They pay the full $500,000. As the factoring company paid $400,000 upfront, this leaves $100,000 in reserve. From this $100,000 the factoring fee and the additional fees have to be subtracted before John will receive the rest of his payment.

- 3% of $500,000 = $15,000 and another 2% (1+1 for two weeks)

- 1% of $500,000 (x2) = $5000 (x2)

- All in all Company A will receive: $400,000 + ($100,000 - $15,000 - $10,000) = $475,000.

That is quite a hefty price tag, naturally, the second fee becomes more problematic as the invoice is paid later and later.

This is why invoice factoring or discounting should only be considered when the circumstances require it and should be reserved for customers/clients that have a tendency of paying in quite a timely fashion. But if customers pay in a timely fashion, there should be no reason to even consider invoice factoring. While that may be the case, there are instances in which even though you expect to be fine just waiting for the payment, a situation might occur in which the money is required faster than anticipated, factoring could be a potential savior.

The difference between factoring and discounting

The most defining difference between invoice factoring and discounting is associated with the recipient of the payment. In factoring, the provider of the factoring service is tasked with managing the sales ledger, credit controlling and ultimately chasing the customer for the payment. This means that with factoring you are theoretically ‘outsourcing’ your invoice, which is a downside.

Your customers/client might feel alienated and feel less inclined to do business with a company that uses factoring services. Perhaps, the Factoring provider will have an aggressive approach to obtaining the payment from the client, or customers will simply be uncomfortable with paying a third party.

Invoice discounting allows you to omit this process, as they are not informed that you have made an agreement with a third party. Clients will stay pay your business directly, and it is up to your business to settle it with the discount provider. The downside to this approach is the fact that you have to pursue your clients for payment, and for settling the financial arrangement with the discount provider.

Conclusion

Invoice factoring or discounting is a great way to stabilize the financial cash-flow of a business. It can help overcome the financial liquidity problems that SMEs experience on a daily basis, and ensure that the business can survive. While such services hold a hefty price tag, they are obtained more easily and have lower interest rates than most loans. They are also extremely useful as they do not burden the business over a prolonged period of time when the invoice is paid, the debt can be settled and there is technically no need for a business to bind itself with the provider.